Overall CPI inflation came in at expectations at 0.2% last month and 2.5% last year. The annual rate was down from 2.9% last month and the lowest annual growth rate since February 2021, indicating that overall inflation is continuing to ease. Core inflation (the subject of this post) beat expectations on a monthly basis: 0.3% vs. 0.2% expected, although the expected annual rate of 3.2%.

See CEA’s thread X for more details, including the fact that housing inflation rose in August and is, as the BLS points out, “the leading factor” in inflation this month. While we are careful not to over-interpret any monthly data point, housing pressure on headline inflation has been ongoing and is clearly related to a decade-long very tight housing market and affordable housing shortage.

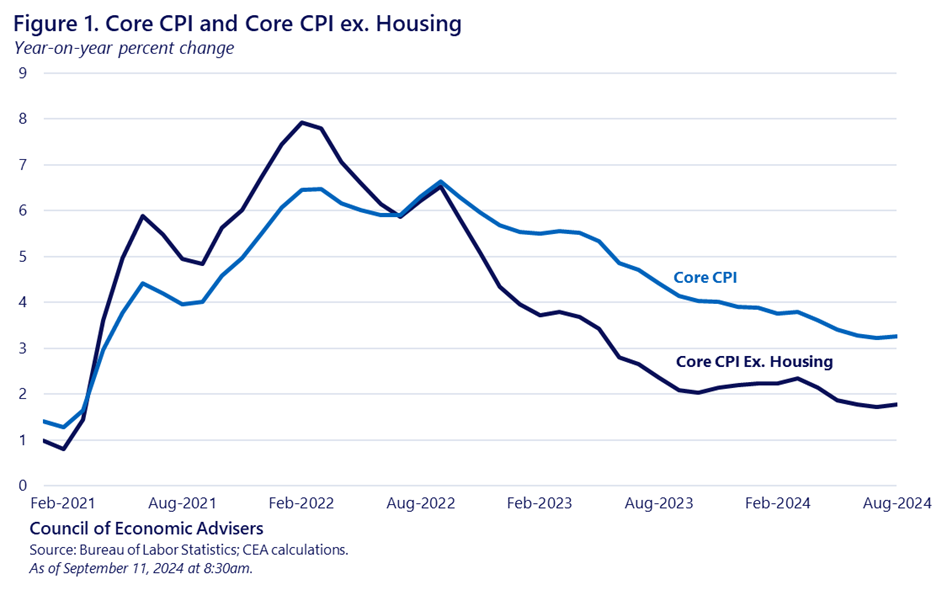

The figure below shows annual CPI underlying inflation with and without housing costs from 2021.[1] It is clear that housing costs have been a major contributor to core inflation since price pressures began to ease. While core inflation, as mentioned, was 3.2% over the past year, underlying prices without housing it increased at a much slower rate of 1.8% as shown in Figure 1. This is due both to the housing inflation rate itself and the fact that housing inflation is about 45 percent of the core CPI basket.

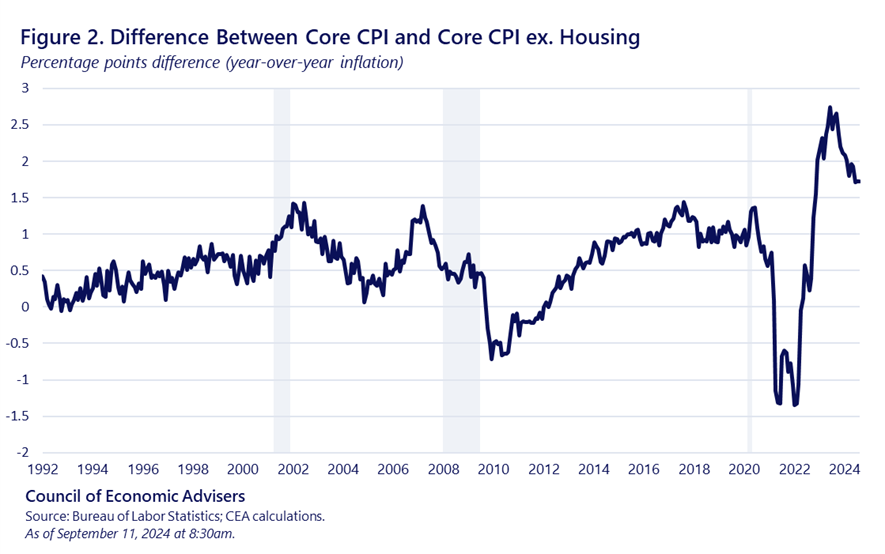

Figure 2 takes a longer-term perspective, showing that the spread between these two measures has been singularly high in recent years.

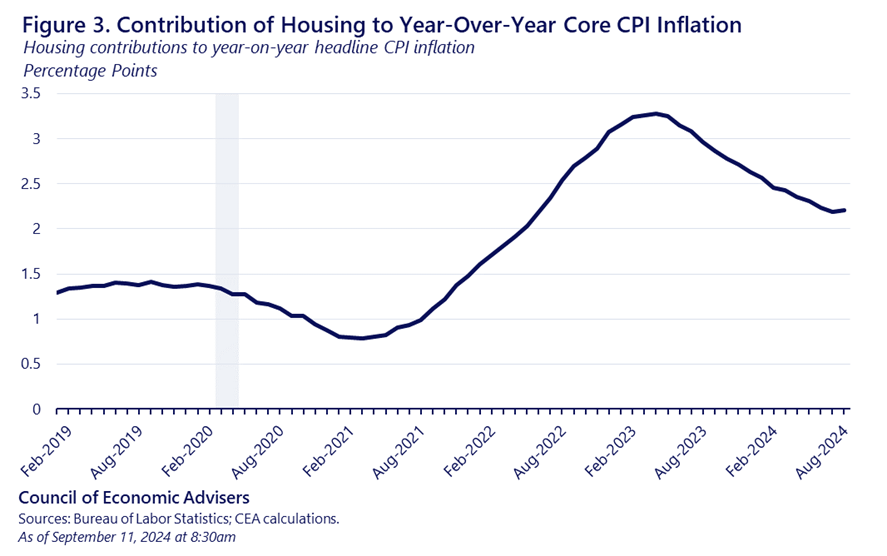

In August, housing contributed 16 basis points (bp) to inflation, accounting for almost all of the 19 bp increase in overall prices. To be sure, non-housing core services remain high, contributing 9bp to headline inflation in August, but this contribution was offset by falling commodity and energy prices this month. Prices of basic goods have fallen in 14 of the last 15 months and by 1.7% over the past year, while prices of basic services outside housing have increased by 4.5% over the past year.

Figure 3 shows the contribution of housing to long-term annual core inflation, once again showing the outsized role of housing in inflation. Fortunately, housing inflation has eased a bit in recent months, falling 3 percentage points from its peak in April 2023.

The point of these calculations is twofold. First, it would be a mistake to conclude that we have not made disinflationary progress in most components of core CPI inflation. In fact, on an annual basis, core inflation is down by more than half from its peak rate of 6.6% in September 2022. And when we take out core housing, it is, as noted, at a relatively low annual rate of 1, 8%.

The second point, however, is what these house price trends show about a structural supply deficit in the US housing market. This deficit, which has evolved over at least a decade, is an issue that CEA has analyzed in great detail, emphasizing the factors behind the shortage. Even more important, we explain the policies that the Biden/Harris administration has proposed to significantly improve this deficit. We believe those measures, which require congressional approval, could quickly begin adding 2-3 million units of affordable housing. This would reduce the affordable housing deficit very significantly, with a commensurate impact on price.

The sooner we can get this agenda going, the better for American households.

[1] CPI inflation is mainly made up of principal residence rent and owner-occupier equivalent rent, as well as smaller categories such as accommodation away from home (ie hotels). We define CPI housing inflation as the combination of primary housing rent and owner-equivalent rent, which accounts for about 95% of housing inflation.

#Role #Housing #Inflation #CEA #White #House